October 2022 E-News: Now is the Time to Reshore from China

As 1H 2022 data demonstrated, reshoring is on a tear. The U.S. is now in a unique position to maintain momentum, rebuild our industrial base and bring more production back from offshore. Imports from China are especially vulnerable. The process is a complex one that requires action by many players. Below are tailwinds and headwinds that will determine continued progress.

Tailwinds

A New Era of Industrial Policy Kicks Off with Signing of the Chips Act “Dani Rodrik, a professor of international political economy at Harvard University, called the law historically significant ‘because it is a sign that we have moved well beyond market fundamentalism and because it shows there is now bipartisan support for industrial policies.’” The Reshoring Initiative (RI) supports the Chips Act. However, the country needs a comprehensive industrial policy to make the U.S. competitive in a broad range of products/industries.

Delivering the U.S. Manufacturing Renaissance McKinsey:The stage is set for a manufacturing resurgence in the United States. $4.6 trillion of exports could shift to regional sources worldwide by 2030. Exhibit 4 analyzes industries by the magnitude and feasibility of shifting. Can the country’s producers make it happen? Harry will be presenting at McKinsey’s related Global Industries Leadership Summit in Chicago on Nov. 17.

POLL: Building American Manufacturing Resilience “CEOs Are Investing In Talent & Technology While Also Reshoring & Nearshoring Their Manufacturing Operations.” A new Xometry Poll with Forbes and Zogby reveals nearly two-thirds (64 percent) of the CEOs say they are currently reshoring or nearshoring their operations, or planning to.

Free Markets Don't Buy Peace The U.S. trade deficit is partially due to the preferential treatment we have given to other countries to encourage their development as democratic nations, thus achieving world peace. This theory has not worked. For example, China continues to enjoy Most Favored Nation status despite its increasingly authoritarian behavior. Russia’s status was revoked in 2022.

Additionally, the USD was 25% overvalued as of Dec. 31, 2021, and has surged another 17% YTD, resulting in a 46% overvaluation. The simplest way to accelerate imports is to reduce the value of the USD using the Market Access Charge.

The Long March Out of China

China is still incredibly competitive in the short run. However, further evidence of increasing risk with China comes to light daily. Basically, everything happening with the country signals red flags for companies sourcing production there. It is not easy to shift production, especially complex electronic assemblies, out of China, but it is better to start the process sooner than later. Reviewing the developments and implications of the risks addressed below is key to making timely sourcing and siting decisions.

Apple’s Tech Supply Chain Shows Difficulty of Dumping China “Covid Zero, deteriorating US-Sino relations pressure US firms. Chips are in the crosshairs as Taiwan-China tensions increase…. Bloomberg Intelligence estimates it would take about eight years to move just 10% of Apple’s production capacity out of China” For all U.S. companies, it is time to start moving now!

China’s dim prospects turn disastrous “China’s debt is expected to reach the equivalent of 275% of its GDP due to massive borrowing and economic slowdown.” If the housing bubble bursts, the subsequent economic melt-down will temporarily be bad news for the global economy. China’s manufacturing costs will come down, but China will still not be cheaper than Mexico or Vietnam. The Chinese economy will flatten or decline. Economic and political instability will lead foreign companies to decide that China is no longer such an attractive market and will shift elsewhere, including to the U.S., Canada and Mexico.

2. Beijing isn't doing enough (to help its economy)

3. China's property market is in crisis

4. Climate change is making matters worse

5. China's tech titans are losing investors

American Health Care’s ‘China Syndrome’ Far too much of U.S. pharmaceutical and medical supplies (including 97% of antibiotics) are sourced directly or indirectly from China. The U.S. government will likely intervene to reduce the dependency.

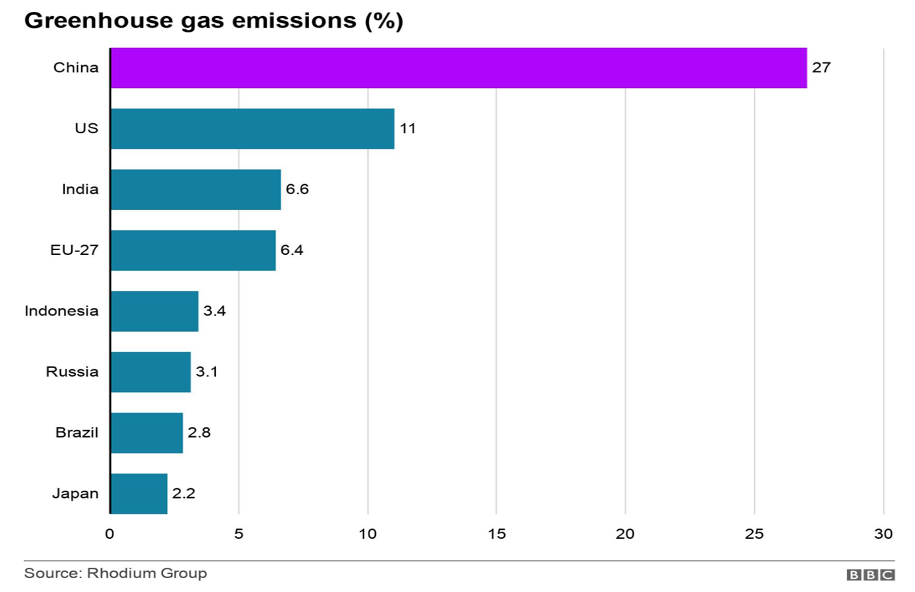

This chart shows China’s huge impact on emissions. It probably does not include emissions from container shipping. Shifting manufacturing to the U.S. reduces emissions due to less coal in our electricity production and due to much lower shipping emissions.

Taiwan Tensions Raise Risks in One of Busiest Shipping Lanes “Bloomberg calculated that almost half of the world’s container ships and 88% of larger container ships transited the Taiwan Strait this year.” Any actual hostilities over Taiwan will have a major impact on supply chains.

Overseeing the recent reshoring momentum should be a national industrial policy, and at the center of it should be a commitment to grow a large skilled workforce. An excellent new book, “Homecoming: The Path to Prosperity in a Post-Global World,” by Rana Foroohar offers a strategic view of how the world will be better with a better balance of localization and globalism. See book review here.

Harry Moser presenting “Manufacturing is Cool” t-shirts as bonuses to executives from Hardinge, Inc., the winner of the 2022 National Metalworking Reshoring Award, at IMTS+ Mainstage. See a recap of the week here.

Why Reshore Reshoring is an efficient way to increase corporate profits, reduce imports and regain manufacturing jobs in the United States. It's also the fastest and most efficient way to strengthen the U.S. economy.