February 2024 E-News: As Geopolitical Risks Mount, Companies Bring Production Closer to Home

Geopolitics and Wars

Present-day inadequacies in the U.S. military make war more likely. The risk of a Taiwan war along with other global conflicts has the potential to impact GDP, corporate profits and civilian safety. These increasing risks demand foresight and preparation by companies and countries alike.

According to AlixPartners’ Disruption Index, 68% of CEOs report that U.S.-China tensions are causing them to change plans.” 94% of SDC respondents say reduction of China sourcing dependence is underway. According to McKinsey's Geopolitics and the geometry of global trade, the use of terms such as “decoupling,” “de-risking,” “reshoring,” “nearshoring,” and “friend-shoring” in corporate presentations increased more than 20-fold between 2018 and 2022. Medius’ October 2023 survey found that 69% of manufacturers are reshoring and 94% of those say the process is successful.

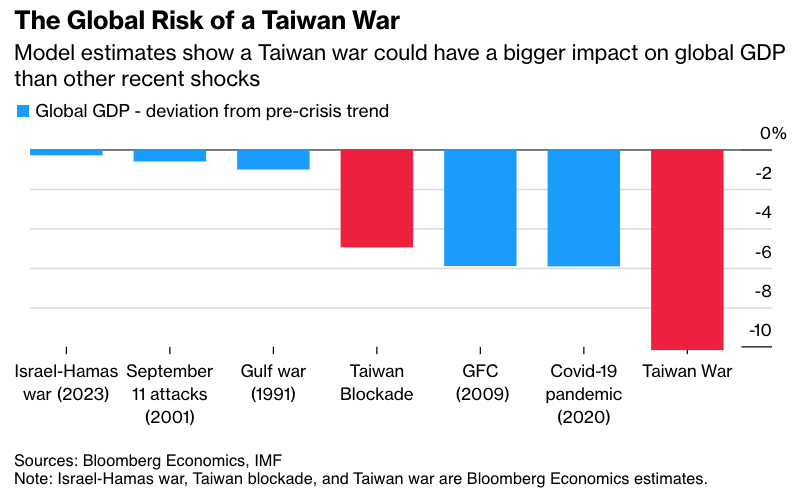

The chart below estimates the impact of war on GDP.

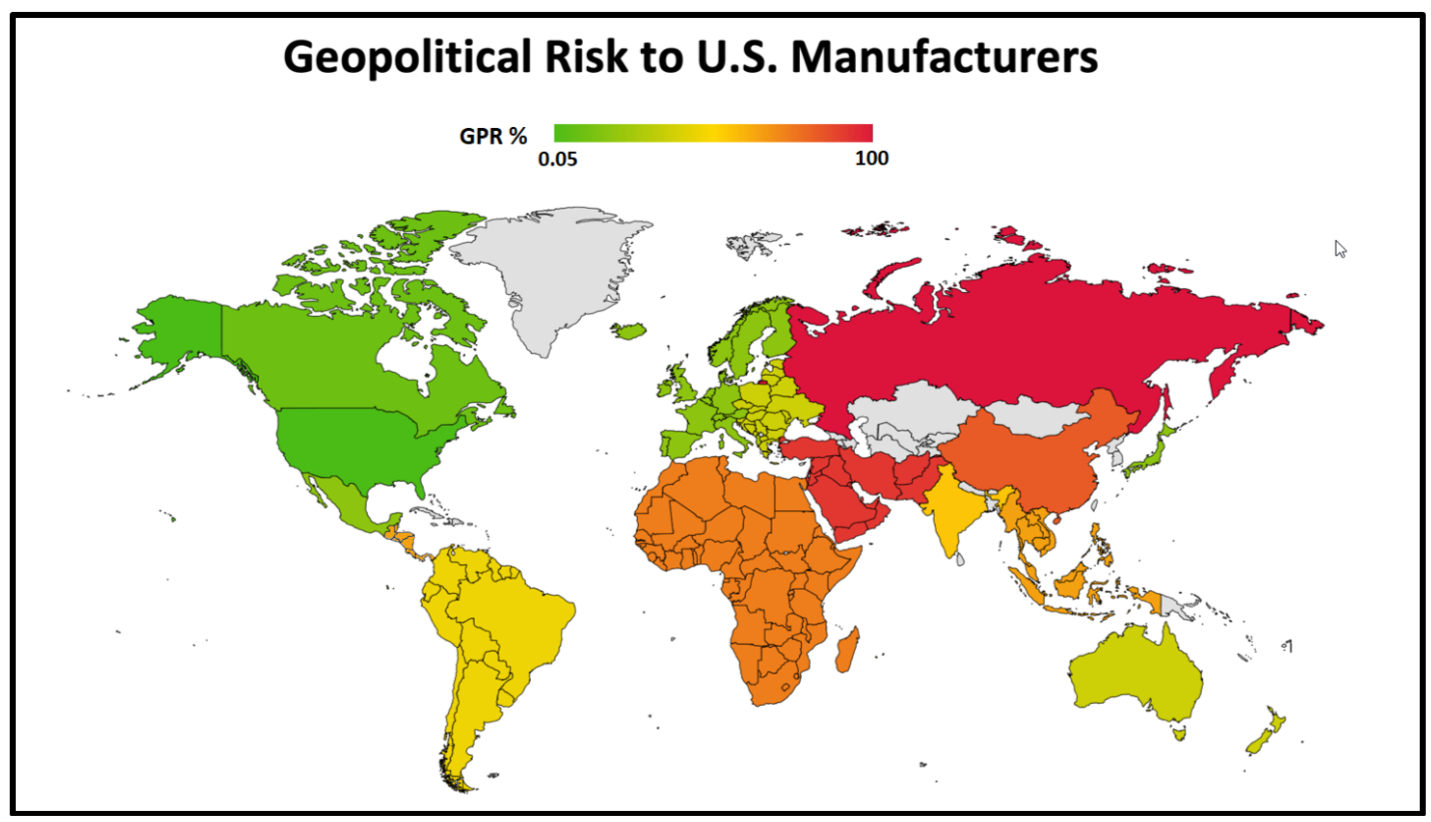

Chief Executive magazine’s survey identified geopolitical risk as the #1 driver of reshoring. Our Geopolitical Risk Index provides companies and the government with estimates of the probability of long-term decoupling of the U.S. from each major supplier country.

“Everyone from Wall Street investors to military planners and the swathe of businesses that rely on Taiwan’s semiconductors are already moving to hedge against the risk. Jude Blanchette, a China expert at the Center for Strategic and International Studies, says interest in a Taiwan crisis from multinational firms he advises has “exploded” since Russia’s 2022 invasion of Ukraine. The subject comes up in 95% of conversations, he said.”

“There’s a higher-level issue than the economy, which is geopolitics,” said Christian Mumenthaler, chief executive of reinsurance giant Swiss Re, which insures risks worldwide. Geopolitics hasn’t been so big an economic threat since the height of the first Cold War in the 1980s.

“Historically, American industry has risen to the task. For nearly a half-century, the U.S. military had access to an enormous and diverse domestic industrial base. Even when supplies ran low at the onset of the Korean War, a heavily industrialized America was able to ramp up within months to generate torrents of weapons that held off vastly larger Chinese forces for the next three years. Today, however, U.S. domestic production capacity is a shriveled shadow of its former self. Crucial categories of industry for U.S. national defense are no longer built in any of the 50 states.” As an example, during WWII my father, Ray Moser, made bombsights at the Singer Sewing Machine factory in Elizabeth, NJ. As far as I can find, Singer no longer has any U.S. factories, so it cannot now produce needed defense material.

Biden needs to rebuild America’s ‘arsenal of democracy’ or risk being unprepared. “Beijing’s buildup should be a blinking red light for Washington. The U.S. defense industrial base lacks the capacity, responsiveness, flexibility and surge capability to meet the military’s needs. Part of the problem is that the U.S. defense industrial base remains on a peacetime footing, despite wars in Ukraine and the Middle East, as well as growing tension in the Taiwan Strait and Korean Peninsula. The U.S. faces a serious shortfall of munitions—especially long-range precision munitions—for a protracted war in the Indo-Pacific.”

Think of it as an insurance premium: “The Kiel study’s authors say that it’s preferable to start reducing exposure to China now than wait for a “much more costly ‘cold turkey’ hard decoupling dictated by geopolitical events.” Companies must take geopolitical risks sufficiently into account in their decision making,” the government in Berlin said in the 40-page document published on the foreign ministry’s website. “The costs of concentration risks must be more strongly internalized on the part of companies so that state funds do not have to be tapped into in the event of a geopolitical crisis.”

Total shipments from China to the U.S. last year fell by 13.1 percent compared to a year earlier, to US$500.3 billion. It is the biggest slump since the agency’s records began in 1995 – more than the declines experienced either during the global financial crisis of 2008-09 or the start of the U.S.-China trade war in 2018-19. The latest shift is not surprising in light of the global effort to reduce supply risk from the region.

New research by investment bank TD Cowen estimates that Apple's loss of earnings because of China is considerable, and in part behind its suppliers moving, or reshoring, to other countries. "Over the last four years since the start of the pandemic, we estimate Apple's revenues have been impacted by over $30 billion." This comes from "undersupplying the market due to production disruptions stemming from component supply, available labor pool, and/or government-mandated movement restrictions." TD Cowen's analysts believe that because of this impact on its manufacturing chain, Apple and its 188 major suppliers are all investing to reshore as quickly as possible — and that they will continue to do so. "We believe these risks are ongoing in nature and that unforeseen environmental disasters could also be included as a non-trivial factor to monitor," write the analysts. "We think the current geographic and labor supply diversification can materially reduce the impact of future production disruptions, which at the peak reduced Apple's revenues by $4-8B per quarter."

They are part of a growing group from China who are crossing the US border illegally, seeking asylum and a better life. About 10 years ago I won a debate in The Economist on whether companies should reshore some manufacturing. Concerning China, I cited a report that many Chinese businessmen were emigrating and shifting their companies to the U.S. I argued that these businessmen had excellent Communist party connections but were still leaving China. So, American businessmen who lack those connections should do as the Chinese do, and leave.

This report has a lot of valuable policy proposals. However, I believe it focuses too much on making China weaker and not enough on making America stronger. The U.S. has a goods trade deficit with 9 of our top 10 trading partners. Unless we become cost-competitive with many countries, we will miss out on most of the work flowing out of China. Our position relative to China will be better if we are stronger.

“The latest AlixPartners’ survey found that total costs are driving part of this trend, as China is no longer the total landed cost leader, especially when adjusted for risk.”

IPC Chief Economist Shawn DuBravac focuses on the economics of nearshoring. Nearshoring’s potential promise is not only to mitigate the vulnerabilities of extended supply lines but also to offer agility in responding to consumer needs, fostering a more adaptable business model.

“Those who insist on forcing a failed policy of unrestricted free trade on the public, in spite of the disastrous effects it has had on American workers, need to check their hubris.”

Reshoring Tips of the Month

Environmental, social and governance (ESG) is an increasingly important corporate performance metric. The simplest ESG strategy is reshoring:

Environmental: About 60% of emissions are Scope 3, i.e. in the supply chain. Across a broad range of products and countries, emissions are reduced by 25 to 50% by making here instead of making there and shipping here. Our revised TCO Estimator will help with the calculations. A recent survey showed reshoring is the #1 action taken to reduce emissions

Social: Each $200,000/year reshored, including in the domestic supply chain, adds one manufacturing job plus multiplier effect jobs in supporting services. No or minimal human rights abuses in manufacturing here.

Governance: The U.S. ranks highly, but not the highest, on governance.

"Regions in the U.S. interior are well-positioned to revive their manufacturing industries with new technology by “deepening,” the application of new technologies to incrementally improve the efficiencies of existing industries. This is the route that Germany, Japan and Korea took as they continuously upgraded their steel, auto, chemical, consumer electronics and related businesses. …By forging a new model of industry-transforming innovation, the heartland can help rebuilding and reshoring of the manufacturing industries that are needed to secure the nation’s economic future.”

The number of companies enhancing their resilience by investing in relocations, automation and digitization will increase in the next three years. This rise aligns with the increasing preference for producing goods within the same selling region, which is anticipated to reach 85% in three years, up from 43%.

Media coverage of reshoring was launched 11 years ago with The Atlantic’s The Insourcing Boom. GE Appliances had been importing a lot of their appliances from China, but reshored several models as highlighted in the article. This success is partially based on GE understanding TCO. CEO Kevin Nolan: “I’ve always said, this is just economics, people are going to realize that the savings they thought they had aren’t real, and it’s going to be better and cheaper to make them here.”

Why Reshore Reshoring is an efficient way to increase corporate profits, reduce imports and regain manufacturing jobs in the United States. It's also the fastest and most efficient way to strengthen the U.S. economy.